Are you aware of the common pitfalls that can erode your wealth and how to prevent them?

In the pursuit of financial independence, it’s not just about building wealth but also about protecting it from erosion. At Trilogy Financial, we understand the critical importance of mitigating wealth erosion to ensure long-term financial stability. Here are ten strategies to help you with asset preservation wealth & tax and achieve your financial goals.

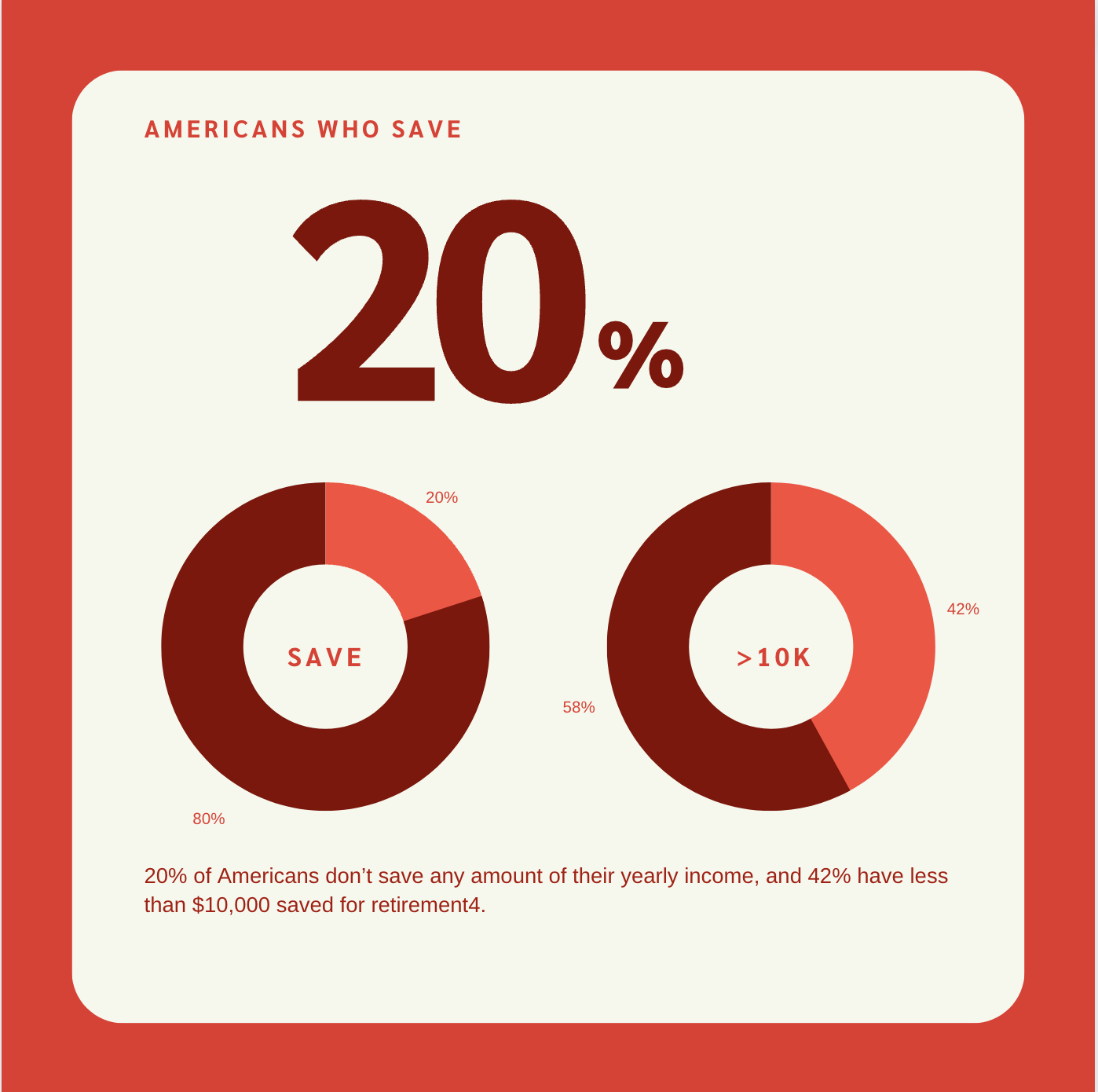

1. Taxes

Taxes are a significant expense for everyone, but High-Net-Worth Tax Strategies can help manage and reduce their impact on your wealth. Consider maximizing contributions to retirement accounts like IRAs and 401(k)s for tax advantages, and explore health savings accounts (HSAs) for additional tax benefits.

Key Tax Strategies:

- Maximize contributions to tax-advantaged retirement accounts.

- Utilize HSAs for medical expenses.

- Consult a tax advisor for personalized tax-saving strategies.

2. Credit Cards

High-interest credit card debt can quickly erode your wealth. Implementing a strategic approach to managing credit card debt can help reduce the financial burden and improve your net worth. One effective strategy for managing credit card debt is to use the debt avalanche or snowball methods.

Credit Card Management Strategies:

- Use the debt avalanche or snowball methods to pay down high-interest debt.

- Consider consolidating debt with a lower-interest personal loan or balance transfer credit card.

- Create a disciplined budgeting plan to avoid accumulating new debt.

3. Depreciation

Assets like cars and electronics lose value over time, impacting your wealth. Adopting a ‘buy and hold’ approach and making strategic purchasing decisions can help mitigate the effects of depreciation.

Combating Depreciation:

- Keep vehicles for longer periods.

- Buy slightly used cars to avoid initial depreciation.

- Invest in assets that appreciate or depreciate less over time, such as real estate or classic cars.

4. Market Cyclicality

Market volatility can cause anxiety, but a diversified investment strategy can help manage the risks associated with market fluctuations.

Navigating Market Cyclicality:

- Diversify your investments across different asset classes and geographies.

- *Implement dollar-cost averaging to manage investment costs.

- Consult with a financial advisor to tailor a diversified portfolio.

*Dollar cost averaging involves continuous investment in securities regardless of fluctuation in price levels of such securities. An investor should consider their ability to continue purchasing through fluctuating price levels. Such a plan does not assure a profit and does not protect against loss in declining markets. (67-LPL)

5. Lack of Diversification

Putting all your investments in one basket increases risk. Diversifying your portfolio across various asset classes and sectors can reduce volatility and potential losses.

Diversification Strategies:

- Invest in a mix of equities, fixed income, and alternatives.

- Use broad market instruments like ETFs or mutual funds.

- Regularly review and rebalance your portfolio with a financial advisor.

6. Unexpected Expenses

Unexpected expenses can disrupt your financial plans. Establishing an emergency fund is crucial to cover unforeseen costs without resorting to high-interest debt.

Preparing for Unexpected Expenses:

- Build an emergency fund covering 3-6 months’ worth of expenses.

- Automate savings to ensure consistent contributions to your emergency fund.

- Adjust your budget to prioritize saving for emergencies.

7. Misaligned Investments

Investing without a clear plan can lead to poor financial outcomes. Aligning your investments with your financial goals, risk tolerance, and time horizon is essential.

Aligning Investments:

- Define clear investment goals and time horizons.

- Educate yourself about different investment types.

- Seek personalized advice from a financial advisor to create Custom Investment Strategies.

8. Procrastination

Procrastination can significantly impact your wealth-building efforts. Starting early and setting achievable goals can make a big difference in your financial future.

Overcoming Procrastination:

- Set short-term and long-term financial goals.

- Use financial tools and apps to automate savings and investments.

- Consult a financial advisor to create a tailored financial plan.

9. Lack of Planning

A comprehensive financial plan is the foundation of successful wealth management. An advantage of effective personal financial planning is that it can transform uncertainty into a roadmap for success.

Creating a Financial Plan:

- Assess your current financial situation.

- Set realistic and specific financial goals.

- Develop a plan that allocates resources towards achieving these goals.

10. Lack of Proper Protection

Unexpected life events can derail your financial plans. Proper insurance and estate planning can protect your wealth and provide confidence.

Implementing Proper Protection:

- Obtain adequate life, disability, and long-term care insurance.

- Create a will and other estate planning documents for Legacy Planning.

- Consult with a financial planner to assess your Financial Protection Strategies.

Conclusion

Preventing wealth erosion is as important as building wealth. By addressing these common pitfalls with strategic planning and professional guidance, you can safeguard your financial future. At Trilogy Financial, we specialize in Comprehensive Wealth Management Services, Retirement Planning for High-Net-Worth Individuals, and long term family wealth planning. Our services also include family wealth protection, risk management positions, and Custom Investment Strategies that protect and grow your wealth. Contact us today to learn how we can help you achieve your financial goals and secure a prosperous future.

Ready to Amplify Your Wealth today?

If you're ready to elevate your financial planning with our professional team, we invite you to schedule a meeting with us. At Trilogy Financial Services, our advisors in Corona are dedicated to crafting personalized financial strategies that align with your unique goals. Don't wait to start your journey towards financial success:

- Schedule a Meeting: Reach out to us to arrange a one-on-one consultation with our financial professionals.

- Give Us a Call: Prefer a quick conversation? Feel free to give us a call to discuss your financial needs and how we can assist. Call Us To Get Started. (844) 356-4934

Schedule a No-Strings-Attached Portfolio Review today and embark on a path to financial success guided by professional advisors. For more information and to schedule your consultation, visit www.trilogyfs.com/yourmoneyamplified. With the right knowledge and professional guidance, the journey of investing becomes an exciting venture towards achieving financial security and growth. This way, you're not just dreaming of an ideal retirement but actively working towards making it a reality.

*There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.