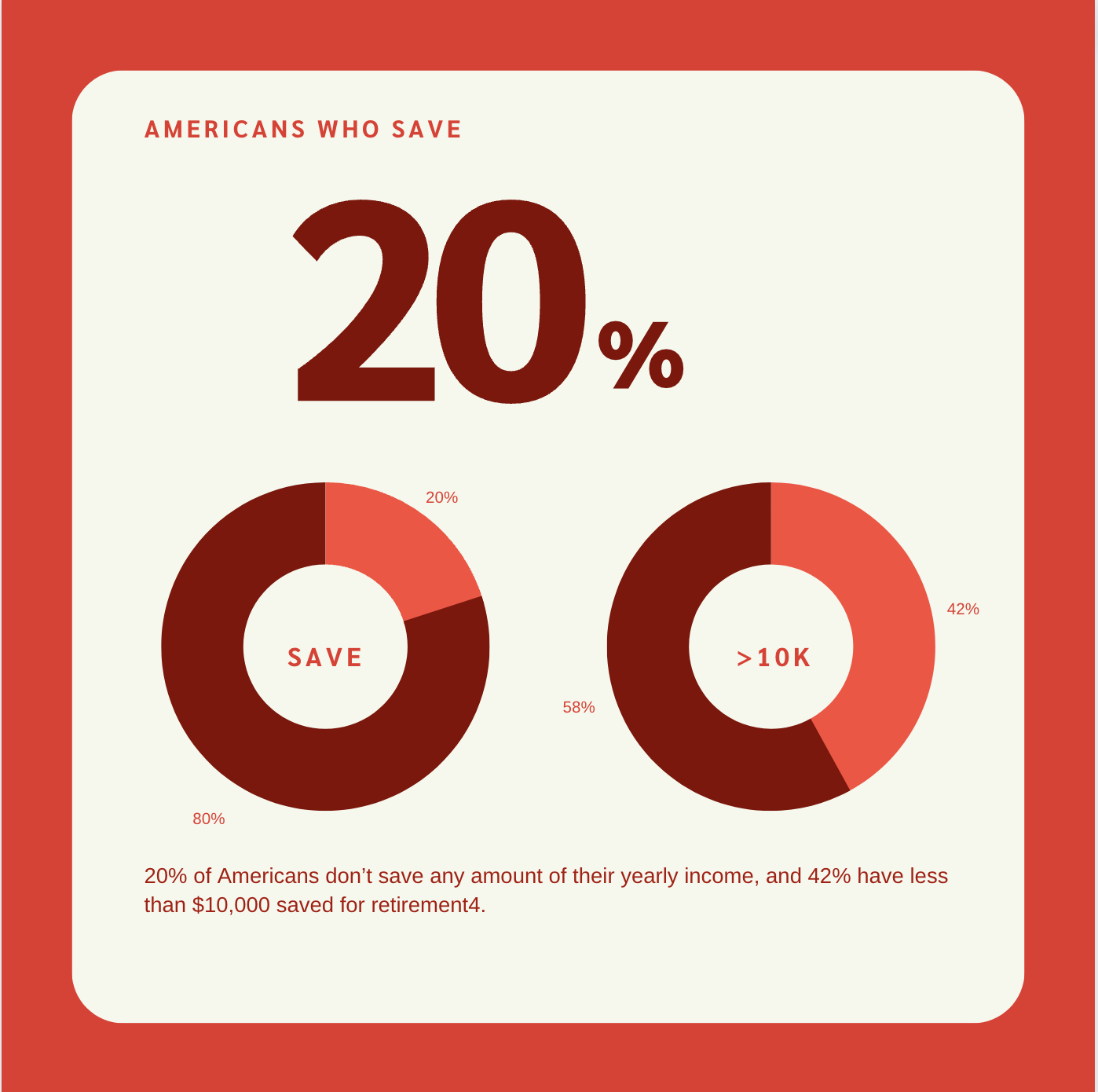

People are living longer – that’s a fact. Unfortunately, all those additional years aren’t always spent in optimum health. With longevity comes the complicated question of how to pay for the necessary health care for those additional years. Costs for unexpected and long-term chronic care are rarely covered by Medicare. People are having to face these costs on their own. Thankfully, the right type of planning can make this task less daunting.

Long-term care can be an overwhelming topic. The statistics are sobering. 52% of people turning age 65 will need some type of long-term care services in their lifetimes, and 14% will need long-term care for longer than five years. With the median annual cost of adult day care averaging $18,200 and assisted living facilities at $45,000, the financial implications can be staggering. It can sound like a complicated topic, but the way to protect you really boils down to three options.

- Self-insure: This is the option that many select by default because they don’t want to think about the possibility of illness creeping into their future. It’s a scary option, which they hope won’t happen to them. However, this option typically leaves them unprepared for the medical costs that eventually do occur.

- Long-term Care Policy: This is a good form of financial protection as it covers your risk but won’t wreck your financial plan. However, the down side with such a policy is that if you don’t use it, you lose it.

- Accelerated Benefit Riders (ABR’s): Lastly, you can invest in life insurance you don’t have to die to use. These riders in your insurance plan will allow you to receive your benefits prior to death due to terminal, chronic or critical illness. The ABR’s will cover your risk, and you’ll still receive the benefit if you don’t need to use it for long-term care purposes.

Now, there is no one-size-fits-all solution. It’s always best to meet with your trusted financial advisor to find the right option for you. Just know that when you do take the time to plan ahead and find the right option for your particular situation, you’re not only providing for your future but also your peace of mind as well.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.