Planning for retirement amid changing market dynamics can be stressful, especially as retirement age approaches. Fortunately, there are a myriad of ways to prepare for it, even if you plan to retire early.

OPTIMIZE YOUR RETIREMENT INCOME

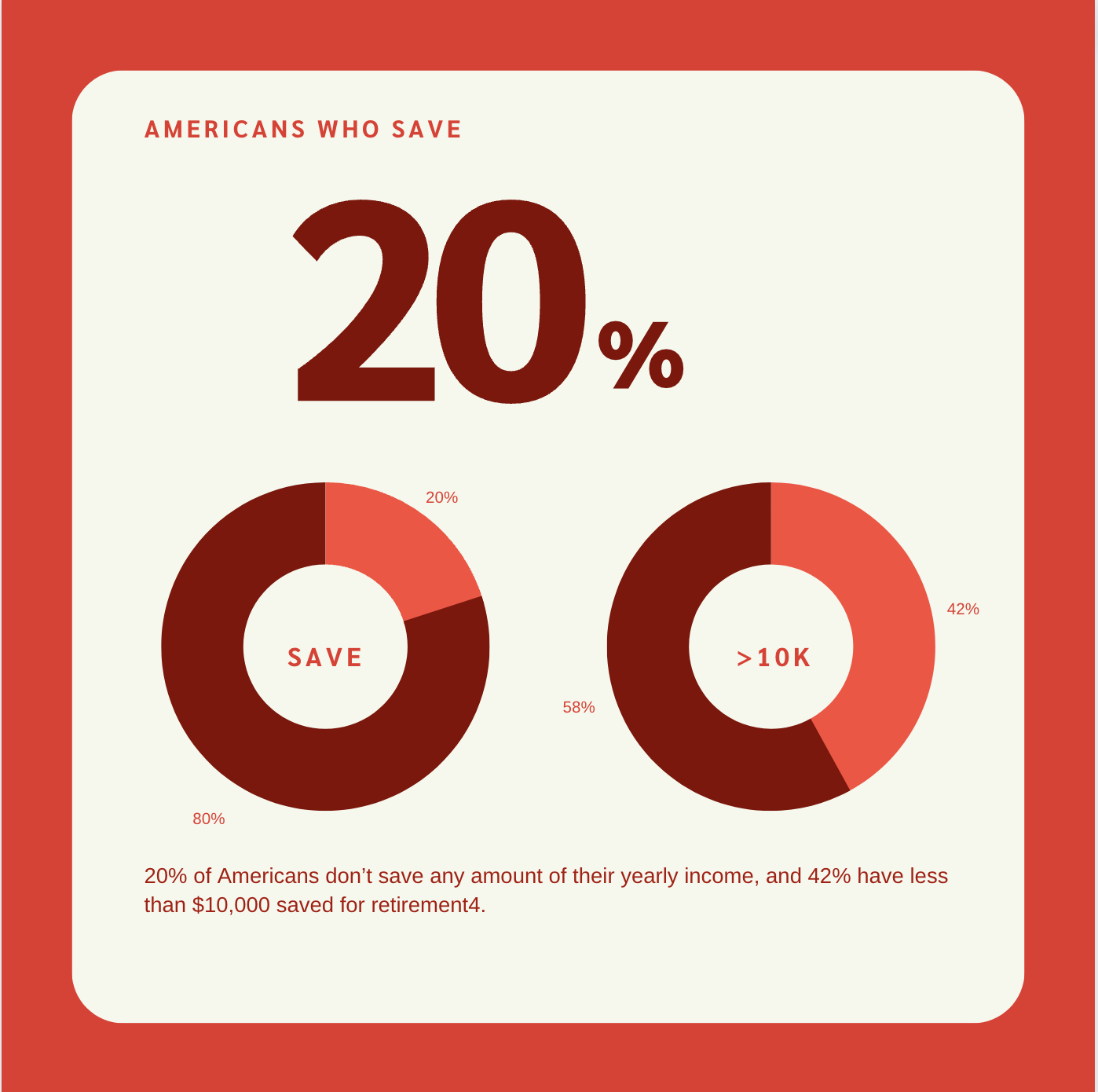

One of our top tips is to optimize your retirement income by setting yourself up with a diversified portfolio that offers a solid return. If you are in your twenties, there is a big opportunity to let compound interest work its magic. If you are in your thirties or forties, compound interest may not be as lucrative for you, but there are still plenty of ways to maximize your returns.

Here are some of the different options available to help plan for retirement:

- SEP IRA – a self-employed retirement plan known as the Simplified Employee Pension (SEP) IRA requires employers to contribute 100% of the accounts' funds and provide equal benefits to all eligible employees.

- 401(k) – An individual retirement plan for which contributions are not tax-deductible, but withdrawals in retirement are tax-free.

- Roth IRA – An individual retirement plan for which contributions are not tax-deductible, but withdrawals in retirement are tax-free.

Each option has its differences, so it is important to work with an advisor to identify which is best suited to your situation and your goals. There’s a lot that can go into your Life Plan and we are here to help.

DEVELOP A BUDGET AND SAVINGS PLAN

Budgeting can make a world of difference. If you haven’t already, establish an emergency fund. This will give you peace of mind and will help pay for any unexpected expenses that may arise. Once you’ve set that money aside, you can plan your monthly expenses, retirement contributions and more with the rest of the income you have.

As you develop this budget and savings plan to get you to your retirement goals, ask yourself the following questions:

- What quality of life do I want to experience in retirement?

- What medical expenses do I anticipate?

- Do I plan on working during retirement?

- Will I have a flow of income during retirement?

These are all important considerations and will help you develop an actionable plan to achieve the retirement lifestyle you dream of.

DETERMINE YOUR TAX BRACKET AND MINIMIZE YOUR TAXES

In retirement, taxes can eat into your available income, leaving you with less to live on. It's important to remember that taxes don't stop once you're retired. Our financial advisors are here to help guide you take steps throughout your working life to minimize your IRS obligations now and later.

The same basic tax brackets that apply to working taxpayers also apply to retirees. Determining your tax bracket in retirement is just like determining your tax bracket while you’re working – which is determined by your filing status and taxable income (income minus deductions).

Common sources of retirement income that are taxable include:

- Distributions from traditional 401(k)s and IRAs

- Investment income

- A portion of your Social Security benefits (in some situations)

- Some pension income

- Income from work (full or part time)

INVEST TO ADD ADDITIONAL CASH FLOW IN RETIREMENT

If building wealth is your goal, the stock market or other investment strategies are common options. Investments such as annuities, real estate investment trusts (REITs) and income-producing equities can offer additional retirement income beyond Social Security, a pension, savings and other investments.

DETERMINE THE AMOUNT OF RISK THAT IS APPROPRIATE FOR YOU

It is important to keep in mind that all investments come with risk. If you are young, you can probably tolerate more risk. If you are in your thirties or forties, however, you might benefit from taking a lower risk approach. This is because people in their twenties have more time to correct and mitigate losses. A financial advisor can help you decide if you would like to take a low-risk, slow-and-steady approach, or guide you through a high-risk approach with the potential of yielding higher returns.

PAY OFF YOUR DEBTS

It’s important to pay off credit card debt and student loans as soon as possible. Systematically chipping away at debt now, can have a significant impact on your future debts and purchasing power.

A mortgage can be looked at as both a good debt and a bad debt, depending on your goals. Many people choose to rent a home to avoid being tied to a mortgage, and others use that property as a cash-positive asset. Depending on your goals, it’s important to discuss each of these approaches with a financial advisor so they can help guide you through something that will ultimately benefit you and your family.

MAXIMIZE YOUR SOCIAL SECURITY BENEFITS

Navigating Social Security income can be complicated, but there are several ways to maximize your social security benefits, including:

- Work for 35 years or more

- Earn as much as you can right up until full retirement age (or past it)

- If you can, wait until you are 70 years old to claim – this can increase your benefit by 8% a year beyond your full retirement age

The goal is to maximize the income you will receive from Social Security, but the answer for you will depend on your age, current income, marital status, spouse’s income, and the age disparity between you and your spouse. With all the complexities to Social Security planning, there is no substitute for meeting with a trusted financial advisor so you can best navigate your life in retirement.

CONSIDER ESTABLISHING STREAMS OF PASSIVE INCOME

It's important to remember that there are multiple ways to set yourself up for prosperity during your golden years.

These include:

- Investing in real estate

- Investing in the stock market

- Starting an ecommerce business

- Writing books

- Earning royalties of any kind

- Investing in collectibles

- Investing in gold and silver

In short, it's best to invest in as many financial assets as you possibly can in order to establish streams of passive income so that you are not solely reliant on one source for your earnings and returns.

ESTABLISH MULTIPLE STREAMS OF INCOME

You may want to consider continuing to work during retirement. This provides many people with a sense of satisfaction and purpose, AND you will be able to keep your benefits.

The earlier you establish multiple sources of income the better. Ideally, at least a few of these would be passive.

You deserve to be comfortable during retirement, and planning for this phase of life right now will likely help you achieve your goals, perhaps even surpass them. You have worked hard for most of your years around the sun, and you deserve to relax and enjoy every moment on your own terms during your golden years.

Why Choose Trilogy Financial

Planning your retirement strategy is important but not something to stress over. If you’ve already started saving, one of our certified financial planners can help you optimize your savings, investing and risk approach so you can live the retirement life you dream. However, if you haven’t started planning for retirement yet, there’s no better day than today!

Our Advisors will work with you to develop a deeper understanding of your alternatives, pinpoint practical needs and make plans for the care you and your family deserve. Please contact us to start your retirement planning today.