In the era of self-directed retirement planning, the need for individualized strategies and informed decisions has never been more pronounced. As you tread into the realm of retirement, engaging with experienced retirement planners becomes crucial to ensure a secure and joyful post-career life. However, the realm of investing can be complex, and making informed decisions is vital for financial success.

If you are looking to make well-informed investment decisions, consider speaking with a financial advisor at Trilogy Financial Services. With the help of qualified professionals, you can navigate the financial complexities that may be hindering your wealth amplifying journey.

Through this expedition, we recommend reaching out to the Financial Planners at Trilogy Financial Services to help guide you through the fog of financial decision. They can help you navigate resources such as the “dont worry retire happy pdf” documents or the more simplified “Retirement for Dummies” documents you might find on the internet when looking for solutions.

Understanding Taxes and Retirement

Let's take a moment to talk about retirement.. It's not merely a phase of life; it's a significant transition that requires meticulous planning and foresight. One of the critical aspects to consider is how might taxes have an impact on your financial plan. A comprehensive understanding of tax implications is essential for effective wealth management, especially when it comes to safeguarding your nest egg from potential tax liabilities.

Wealth Management Strategies

Engaging in astute tax and wealth management strategies is paramount in preserving and growing your retirement corpus. By exploring various tax-advantaged retirement accounts and consulting with professional tax advisors, you can better prepare for the tax implications that come with retirement. This proactive approach not only keeps your financial plan on track but also paves the way for a more secure retirement.

Smart Retirement Options

As you delve deeper into the retirement planning process, exploring smart retirement options becomes a priority. These options could range from choosing the right retirement accounts, investing in tax-efficient funds, to exploring annuity products that provide a steady income stream. The aim is to build a robust financial portfolio that aligns with your retirement goals while minimizing tax liabilities, thereby ensuring your savings not only last but grow throughout your retirement.

Real-world Case Studies

- Transitioning into Retirement: Curt from De Pere, WI, started strategizing for his retirement alongside his wife after lengthy careers in public service, with the assistance of a Financial Planner.

- Early Retirement Evaluation: Stephen and Nicole evaluated an early retirement package to manage taxes efficiently during their transition into retirement.

- Career Change and Retirement Planning: Susan and Chris transitioned from high-profile music industry jobs to retirement, achieving their goals with the aid of First Wealth.

- Long-term Savings Strategy: Jim and Cathy’s story illustrates the importance of long-term savings and debt management, having saved $750,000 in a 401(k) and $300,000 in savings over their working years.

The Bright Side of Retirement

Planning for retirement isn't solely about numbers and finances; it's also about envisioning a happy, fulfilling life post-retirement. Infusing humor and a positive outlook towards this life-altering phase can make the journey enjoyable. A funny, happy retirement is indeed a product of sound financial planning paired with an optimistic outlook.

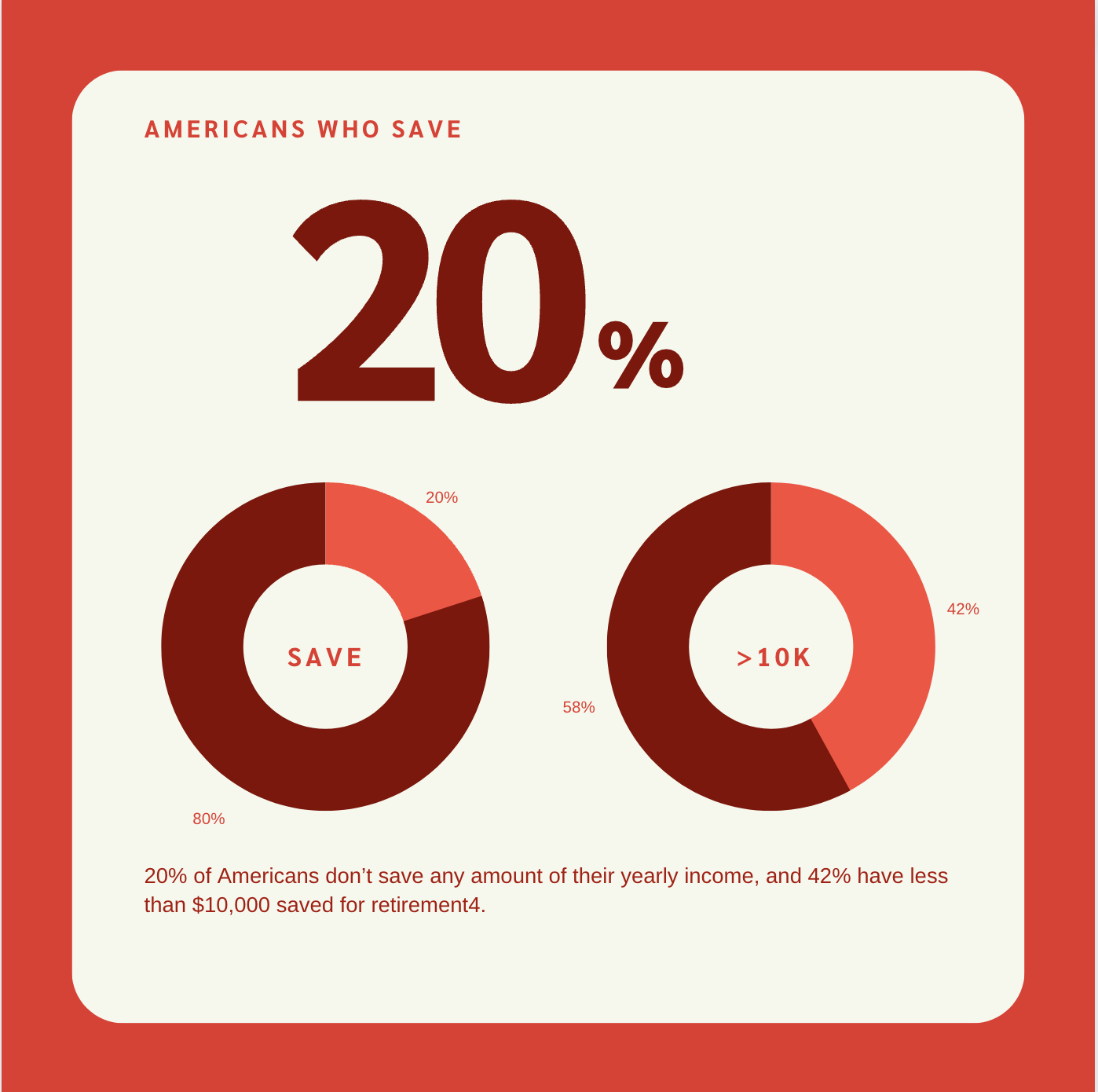

Key Retirement Statistics

- Gender Disparity: Only 17% of women feel on track to meet their financial goals compared to 26% of men.

- Retirement Account Investments: Americans had invested $6.8 trillion in 401(k)s and $12.5 trillion in IRAs as of the first quarter of 2023.

Professional Insights

Professional insights add another layer of credibility to the smart retirement planning narrative. Jim Barnash, a Certified Financial Planner with over four decades of experience, emphasizes the importance of meticulous retirement planning. Understanding complex financial concepts such as the ‘Sequence of Returns Risk' is also crucial as per experts' advice. Moreover, strategic moves endorsed by financial experts can significantly enhance the possibility of retiring as a millionaire, as discussed in a recent piece on Nasdaq.

Planning for the Unexpected

To further aid in your retirement planning, establishing an emergency fund is advisable. An emergency fund serves as a financial buffer, ensuring you have the resources to cover unexpected costs. Having three to six months' worth of living expenses in your emergency fund, which can be adjusted based on your unique financial situation and risk tolerance, is a common goal provided by financial planners.

Leveraging Modern Technology

Lastly, as the digital age continues to evolve, leveraging modern technologies can also play a significant role in your retirement planning process. With the aid of new tools, you can access personalized financial advice, explore various retirement scenarios, and receive insights that empower you to make informed decisions towards a secure and happy retirement. These tools can aid in personalizing your retirement planning process, offering insights and scenarios for better financial decision-making. We recommend speaking to a Financial Planner for a full rundown.

Conclusion

Smart retirement planning is a multi-faceted endeavor that demands a blend of financial acumen, forward-thinking, and a zest for life. By embracing a holistic approach towards retirement planning, you not only pursue your financial future but also set the stage for a joyful and fulfilling retirement. The journey towards a secure retirement begins with the right financial planning, educating oneself on the financial landscape, and making informed decisions that align with your values and retirement goals.

Instead of spending years mastering finances on your own, partnering with those who have already traversed the financial landscape can fast-track your financial success. A dedicated financial advisor from Trilogy Financial Services can work with you to make your money work smarter and harder, simplifying the financial intricacies that have been keeping you up at night.

You can schedule a no-strings-attached portfolio review today and embark on a path to financial success guided by professional advisors. For more information and to schedule your consultation, visit www.trilogyfs.com/yourmoneyamplified. With the right knowledge and professional guidance, the journey of investing becomes an exciting venture towards achieving financial security and growth. This way, you're not just dreaming of an ideal retirement but actively working towards making it a reality.

*There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.