There is one area of planning that gets glossed over, even by the many responsible people: long-term care planning. For so many, it is difficult to plan for something that seems so far removed from their current existence. Many also assume that their current health insurance or Medicare will cover most expenses associated with long-term care. Unfortunately, these mistakes leave them ill-prepared for the expensive reality.

As the US government estimates 70% of individuals who are currently 65 “will require some form of long-term care”.1 Therefore, this is more of an eventuality for most folks than it is a possibility. When an individual’s health starts to decline, hopefully, multiple levels have been put into place. Not only should you be concerned with who will care for you physically, you must all consider who will care for your finances.

Physical Care –The costs for long-term care can be surprising for many, with the average 65-year-old paying approximately $138,000 over his/her lifetime.2 As mentioned earlier, Medicare or private health insurance rarely covers all types and expenses of long-term care. Medicaid assistance varies by state and requires that an individual “must spend down his or her assets and meet other criteria.”3 Additionally, It is important to talk with your loved ones about long-term care options, not only about what one can afford but equally as important, what one prefers.

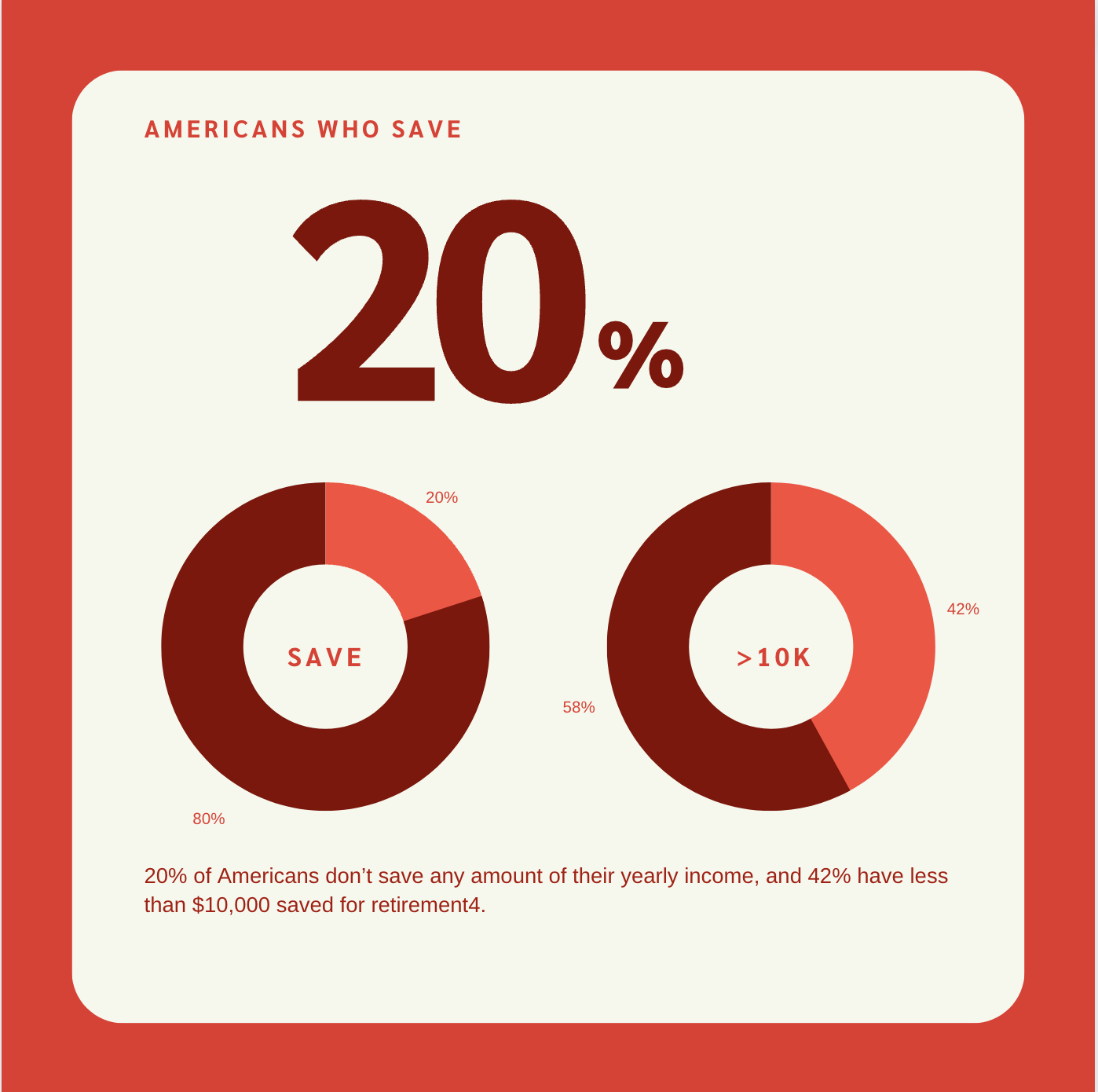

Ultimately, many end up paying for long-term care from their own finances – 50% according to the Bipartisan Policy Center report.4 To protect your finances and the finances of your loved ones, it is vital to prepare for these possible scenarios. There are many long-term care insurance policies that can provide you the assistance your particular situation needs. The premiums for these policies are much more affordable the younger you are. While some of these policies can get a bit confusing, a financial planner can easily go over these policies and help you determine which one would be best for your particular situation.

Financial Care – The key to financially protecting a client in declining physical or mental health lies in teamwork. The team, which consists of their financial team members (financial planner, tax professional or estate planning attorney), delegates and medical professionals. While we all continue to focus on our own particular role and duties, maintaining a professional relationship does give us the opportunity to share any concerning or unusual behavior concerning our client, as well as execute things quickly and as close to the client’s wishes as possible. Equally important is a Durable Power of Attorney (DPA), which legally allows an individual to designate someone to make financial and medical decisions on their behalf should they become mentally incapable to do so. Having these safeguards in place can save on time and hassle should health matters deteriorate and allow your delegate to focus on more pressing issues.

When so many of us pride our independence and self-reliance, declining health issues can be downright scary. I understand this well as I do my best to set my clients up for financial independence, so they can create the life they want to live. When circumstances step in and disrupt your life, it’s vital to know that you have people to rely on and safeguards to protect you.

3. https://www.consumerreports.org/elder-care/elder-care-and-assisted-living-who-will-care-for-you/