Don’t we all just love the holidays? Having a nice, large Thanksgiving meal with close family and friends? Unwrapping presents during Christmas or Hanukkah, seeing the big smiles on the young kids and grandkids as they rip open that favorite toy they begged for? It may be pure bliss during the months of November and December, but come January and February, when those credit card statements come in, the stress starts to set in.

According to the article here, the average person takes more than five months to pay off that holiday debt. Many more carry that into the next holiday season, hence carrying it indefinitely and having it snowball out of control. Many people just make the minimum payment on credit cards throughout the year, and then when the holidays come about, go crazy with buying up everything, their balance goes up, and so does that minimum payment, which they soon cannot afford to pay. Defaults on credit cards and people trying to do balance transfers or debt consolidation soon become the norm and the house of cards (literally) soon falls.

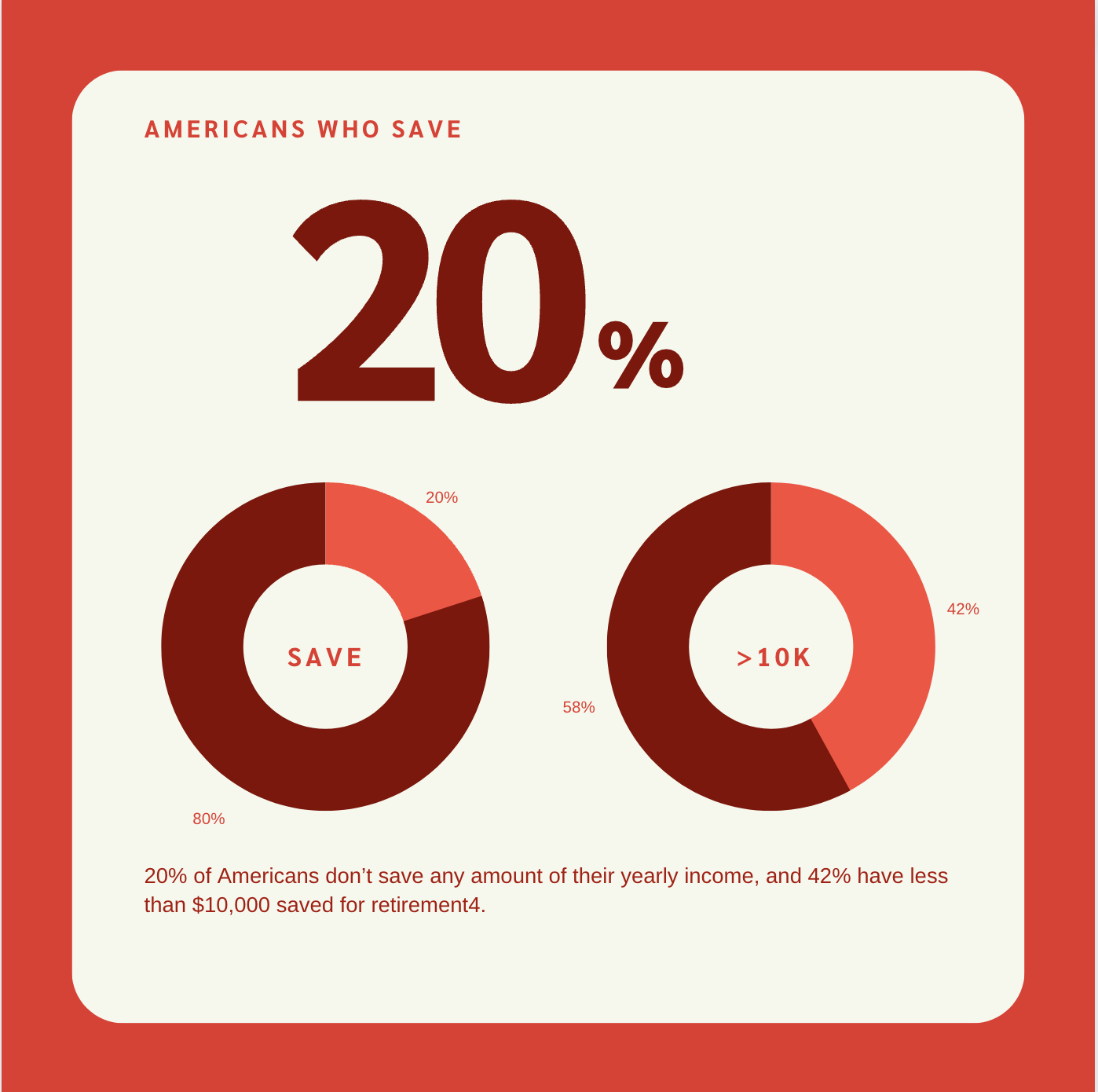

44% of people surveyed stated that they were stressed out because of that extra holiday debt. Among all age groups, Millennials were most likely to go into debt around the holidays. People ages 24-35 were most likely to say they went into debt this holiday season with a rate of 14.3%. With the exception of 45-54-year-olds, the likelihood of going into debt decreased with age. Seniors were least likely to say they went into debt, with a rate of 7.6%.

So how can we mitigate or eliminate this holiday debt altogether?

Start a holiday-saving account: Set aside a holiday or Christmas budget at the beginning of each year! The problem that many people run into is that they do not set a holiday season budget and just spend, spend, spend. We have many clients who save anywhere from $50-200/month starting in January, so that they have their full budget come the 4th quarter. Or, if you are out shopping throughout the year and see a great sale on something that a family member or close friend would like, feel free to buy it, to pace yourself. If it’s within the budget, you should be ok.

Change your tax withholdings: It’s also a proven fact that many people over-pay their taxes throughout the year, over-withholding on their paychecks. The average person pays their amount of taxes by the spring or summertime, and the rest of the year is just spent paying more to Uncle Sam, lining his pockets. We have had many clients who come through our office in the 3rd or 4th quarter, and after we look at their tax returns for the previous year, as long as everything is a constant, we ascertain that they have already paid all of their taxes for the year. They can then increase their withholdings on their paycheck, thus bringing in more income monthly, to allow them to pay for the holiday’s cash. Solution: no post-holiday blues. Then, come January, we would review the client’s situation again, many times working alongside their CPA, to help them get to more of a point of breaking even or getting just a small tax refund back at tax time. This would allow them to better plan out their budget for the year.

Can you change your schedule: Other things to consider to have a credit card-free holiday is to work overtime, if your job allows it, or if you get a bonus throughout the year, to set that aside for the holiday season. But don’t count on it, as you can’t always rely on bonuses, commissions, or pay raises to occur when you want them to.

If you are a people-person and don’t mind strangers in your car, consider driving for Lyft or Uber. I believe they offer tiered bonuses if you complete a certain amount of rides during your first 30 days of working and always have promotions going on. That’s an instant quick bonus for one or two months of work. Many retailers, as well as Amazon, hire hundreds or thousands of seasonal part-timers, to help with the holiday rush. Maybe you can even use that employee discount at that retail store you’d be working at to get a good deal on some presents. UPS and FedEx also hire extra drivers and warehouse employees to sort through all of those packages that are being delivered the last two months of the year.

Conclusion: Get creative and don’t get complacent. You can do this!

Action items:

Understand where your money actually went.

There are many great apps out there which can track your spending throughout the year, and help you stay up on things, so things don’t spiral out of control

Set a realistic budget of what you will spend on family, friends, co-workers, and even clients, if it merits it in your situation, so you don’t break the bank

Work with a trusted financial advisor/coach that can hold you accountable on your spending, so you can keep pace to reach your financial goals

Good luck and let us know your progress! Enjoy the holidays and create some lifetime memories!

[1] http://www.magnifymoney.com/blog/featured/americans-holiday-debt-added-1003-average-year/