If you're one of the millions of Americans who received, or are expecting to receive, a tax refund, you are probably trying to decide how to spend it. The average refund this year is around $3,000, a nice chunk of change to throw at one of your goals. Rather than impulse buying that new Apple iWatch or splurging at Sephora, make the best use of this windfall by putting it towards improving your financial situation.

Build Up An Emergency Fund

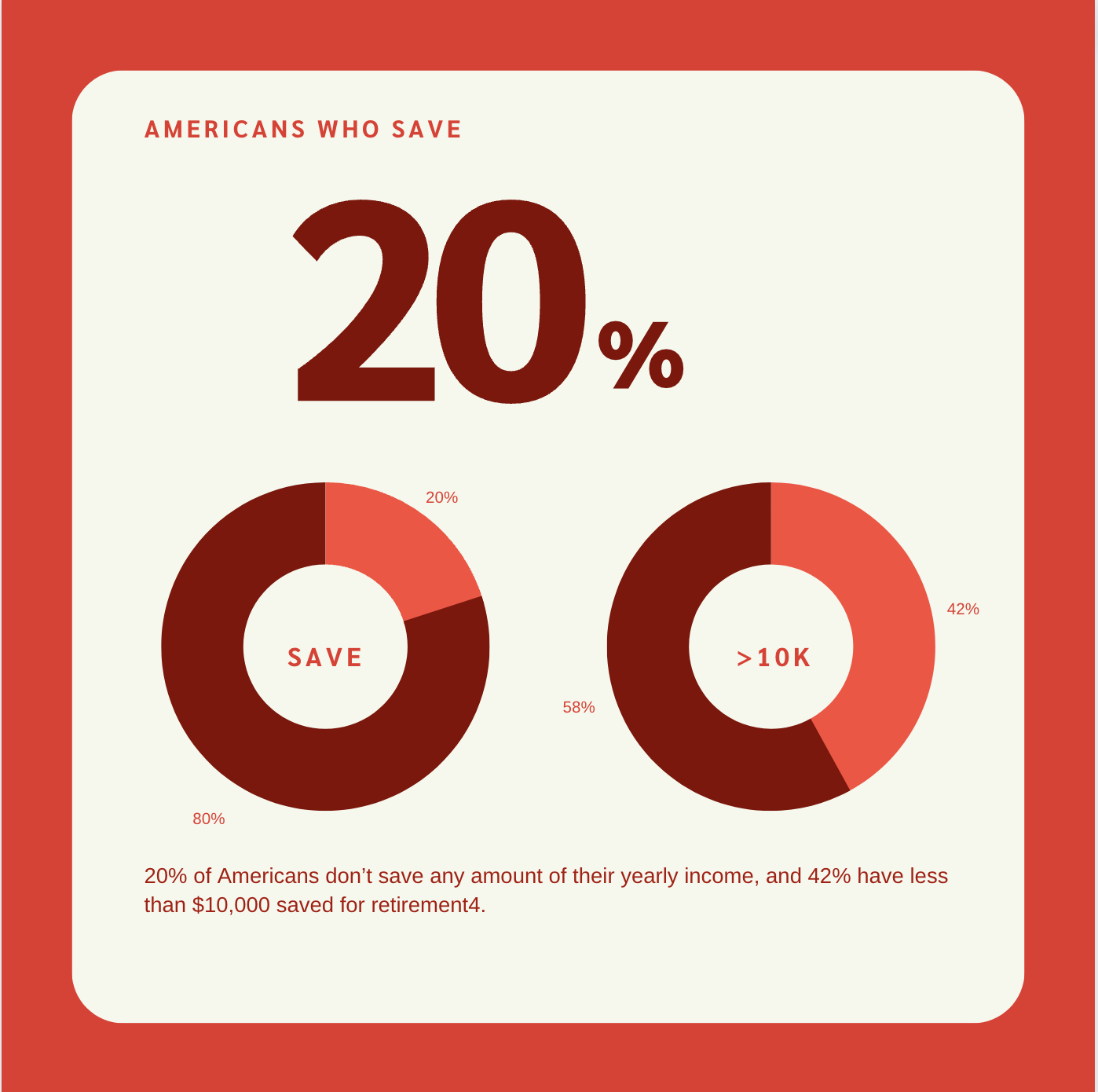

Some very good friends of mine woke up recently to find that their downstairs had flooded from a burst pipe on the second level. They had to rip up their hard wood floors, replace furniture, and even replace some of the walls. Luckily, their bedroom and their child's nursery was spared, but THIS type of unexpected event is exactly why you need an emergency fund. If they didn't have cash readily available in a savings account, they might have been tempted to put charges for repairs and replacements on a high-interest credit card. Depending on your situation, you should ideally have 3-6 months of regular expenses in the bank. Use your tax refund to start, or top off, your rainy day fund.

Pay Off Debt

The power of compounding interest can work in your favor when investing, but it can also cause debt to grow faster than you might think. Credit card companies apply their interest fees to the amount that you owe initially. But every month (and sometimes every DAY!) after that, the compounding interest will apply to the principal, as well as the previous month's interest. If you want to apply the snowball method, apply your refund to the smallest account you can close out. Alternatively, you can use the “Avalanche” method, and put your refund towards the card with the highest interest rate. Paying off the smallest account might feel good, but if you have double digit interest accruing on a card, get that debt paid off as fast as you can. Take the windfall from your refund and put it towards cleaning up your personal balance sheet.

Fund an Individual Retirement Account

IRAs are one of the greatest savings vehicles you can have for retirement. These vehicles allow you to invest in the market outside of any employer-sponsored plans (like a 401K) with tax-free growth (no capital gains!) until retirement. There are two types of IRAs that are available to the general public: Roth IRAs and Traditional IRAs. With a Roth, you contribute post-tax dollars and don't have to pay income taxes on any distributions in retirement. There is, however, a phase-out limit based on income. With a traditional IRA, you do pay income taxes on distributions in retirement. However, contributions made could be tax-deductible for that tax year (contributions made from January 1st of the current year through April 15th of the following year). As of now, individuals can contribute up to $5,500 per year ($6,500 if you’re age 50 or older), or your taxable compensation for the year, if your compensation was less than this dollar limit.

Monetize Other Financial Goals

Planning to take a big family vacation to Disneyland in 5 years? Dreaming of owning a house but need to build up a sizable down payment? Wondering how you are going to pay for your pre-teen's college tuition? If you have any intermediate goals (prior to retirement), consider opening a brokerage account to help your money grow more efficiently. Statistically, the stock market has more up years than down, and historically, has recovered from those down years relatively quickly. If you have time on you side, consider monetizing these goals by participating in the market at a level that is in line with your risk tolerance.

But If You Must, Splurge…A Little

If you just can't help it, take a small percentage of your refund to treat yourself. Whether it's a nice dinner, a manicure, or checking out a movie with your spouse, take a minute to blow off some steam. Keep this amount small though as the path to wealth is paved with good decisions. Start making good habits today to delay gratification and secure a financial safety net in your future.